"Defining Ultra-Luxury: Establishing Brand Standards Amid Market Diversity"

& the need for a private members listing platform

This document has been created to highlight the need for a brand standard for Ultra-Luxury properties. The brand standard is almost impossible to generate or articulate for non-luxury, even mid-range and high-end luxury villas and chalets. Such is the wide diversity of local standards, architecture, guest expectations, amenities and service. The same applies to the vast range of brand and independent hotels, except at the very high end.

Ultra-luxury, however, is a much more refined product and can be elevated above this diversity of accommodation. This accommodation, hotels, villas or chalets is booked by the world’s wealthiest people, of whom over 70% are self-made and who are also the most philanthropic.

In the vacation rental market, the word luxury is undoubtedly overused. As the world evolves through technology and moral and environmental values, we begin to see a transition in the noun’s meaning. Also, one person's luxury could be another person's squalor; such is the polarisation of wealth in the 2020s.

If you want to avoid all the analysis and categorisation, jump to the conclusion, then move to section 8.

Content:

- 1. Definitions

- 2. Luxury is evolving

- 3. Luxury Hotels

- 4. Ultra-Luxury Hotels

- 5. The Villa and Chalet market

- 6. Accommodation grading standards

- 7. Ultra Lux Villas and Chalet Standards

- 8. Whale Sharks vs a UHNW Villa and Chalet Collection -The need for an exclusive listing portfolio.

1. Definitions

Luxury is commonly defined as “a condition of abundance or great ease and comfort: sumptuous environment.”

Ultra-Luxury: It is essential to differentiate this definition, requiring a very bespoke narrative.

In the context of hospitality, Ultra-Luxury accommodation surpasses traditional luxury standards in terms of amenities, service, and overall experience. The accommodation offers unparalleled personalised service, privacy, and attention to detail, with exclusive amenities and facilities designed to cater to the most discerning guests. Ultra-Luxury accommodation is characterised by its exceptional craftsmanship, opulent design, and meticulous attention to every aspect of the guest experience, aiming to provide an unforgettable and indulgent stay for its affluent clientele.

2. "Luxury” is evolving

The traditional definition of luxury, characterised by opulence and excess, is evolving, especially among younger generations like Millennials and Gen Z. Their understanding of luxury often revolves around values rather than material possessions. They prioritise sustainability, health, and social responsibility, leading to a more conscious approach to consumption. This shift has influenced both consumer behaviour and business models.

The new luxury emphasises quality over quantity, timeless products over fleeting trends, and accessibility for more people—concepts such as sharing instead of owning, membership and experiential offerings, and knowledge and transparency from brands.

Democratising luxury, well-being, work-life balance, and digitisation are critical components of this evolving definition. Overall, luxury is now often seen as a lifestyle choice that encompasses positive change for individuals and the planet.

This is a growing ecosystem, yet the more specific non-FMCG luxury market is often less aware of the trends and coming expectations. Consider sustainability as a significant factor. Flying to exotic destinations and overindulging is constantly at odds with the global necessity to reduce the carbon footprint and promote this. People are increasingly travelling; it’s human nature, but those responsibilities lie with all of us.

As we will see later, the Ultra-Luxury market has a higher percentage of the older generation, yet this is changing, too.

Luxury is a growth market

Despite travel and tourism challenges; the luxury accommodation market has seen explosive growth within the hotel industry, which has more data available. We will look at these markets (Luxury and Ultra-Luxury) separately to illustrate the differences in approach and atmosphere. We will also use the hotel sector to demonstrate the surge in luxury and Ultra-Luxury markets.

3. Luxury hotels

In this category, high net worth individuals (HNWI) are categorised as having over $1m worth of assets.

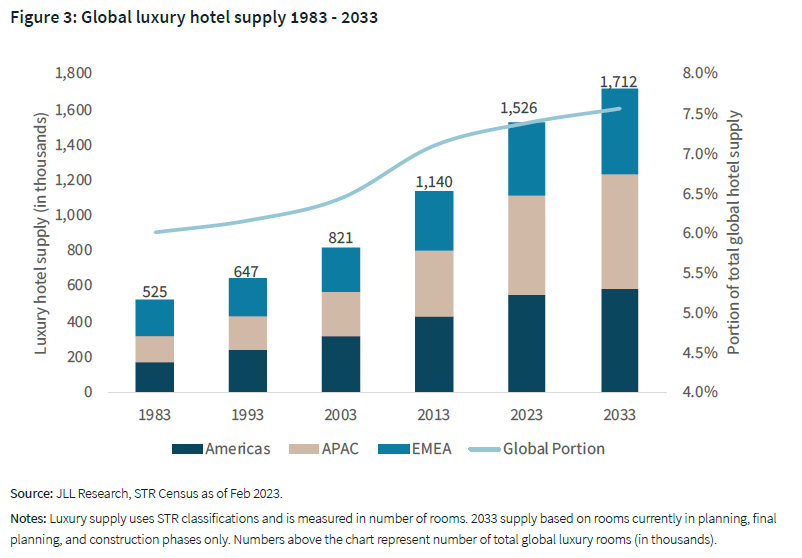

Over the past four decades, the luxury hotel industry has witnessed remarkable growth, marked by a surge of over one million rooms. Where hotel growth accelerates, so follows rentals and the contest on price vs value.

Although constituting a mere 0.3% of the global populace, HNWIs wield substantial influence in the travel sector, contributing around 36.0% of total international travel expenditure and nearly 70.0% of luxury travel spending.

This expansion hasn't gone unnoticed by investors, who are increasingly attracted to luxury hotels as a solid institutional investment. Furthermore, shifting consumer preferences have opened up new avenues for investment, leading traditional luxury hotel brands to venture into unconventional sectors like residential properties, yachting, and exclusive member clubs.

These organisations aim to control every aspect of the traveller's journey. As global connectivity increases and travellers crave more personalised experiences, the luxury hospitality sector is poised for further evolution and expansion.

An expanding supply is meeting the rising demand for luxury hotels. Over the last four decades, luxury hotels have claimed a progressively more significant portion of the global hotel market, a trend projected to continue into the next decade. By 2033, it's anticipated that there will be 1.7 million luxury hotel rooms worldwide, comprising 7.6% of the total hotel inventory.

4. Ultra-Luxury Hotels

Over the past decade, there has been a notable increase in ultra-high-net-worth individuals (UHNWIs), defined as those with a net worth of at least $30.0 million, just below that are very high net worth (VHNW) individuals – $5 million to $30 million net worth.

While this demographic tends to be older, with 89.8% over 50, there's an expected shift towards a younger demographic in the coming years, especially in regions like India, Asia, and the Middle East.

These individuals prioritise philanthropy, particularly in education and sustainability, alongside their passion for travel, which is seldom purely recreational due to their professional commitments.

As a result, they highly value privacy and connectivity in their travel experiences, eschewing the spotlight and preferring discretion over extravagance. This inclination has driven the proliferation of Ultra-Luxury hotels, distinguished by their exceptionally personalised service and exclusive amenities.

Leading brands such as Aman, Four Seasons, and The Ritz-Carlton epitomise this sector, currently offering 197,000 Ultra-Luxury hotel rooms globally, with a further 40,000+ in the pipeline.

This market is blossoming despite global poverty being a significant problem and sustainability concerns being so present.

5. The Villa and Chalet Market

The Trends

Before the OTA consolidation of smaller marketplaces, the short-term rental market was more fragmented in collective marketing opportunities. Now, we witness these major corporations targeting luxury accommodation for numerous reasons: urban legislation, higher per-booking income, often fewer complaints, greater interest in the sector, etc.

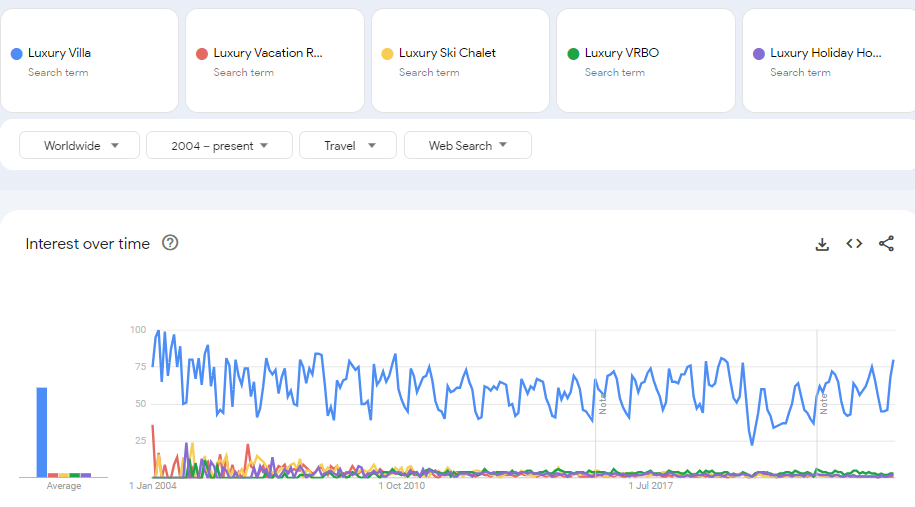

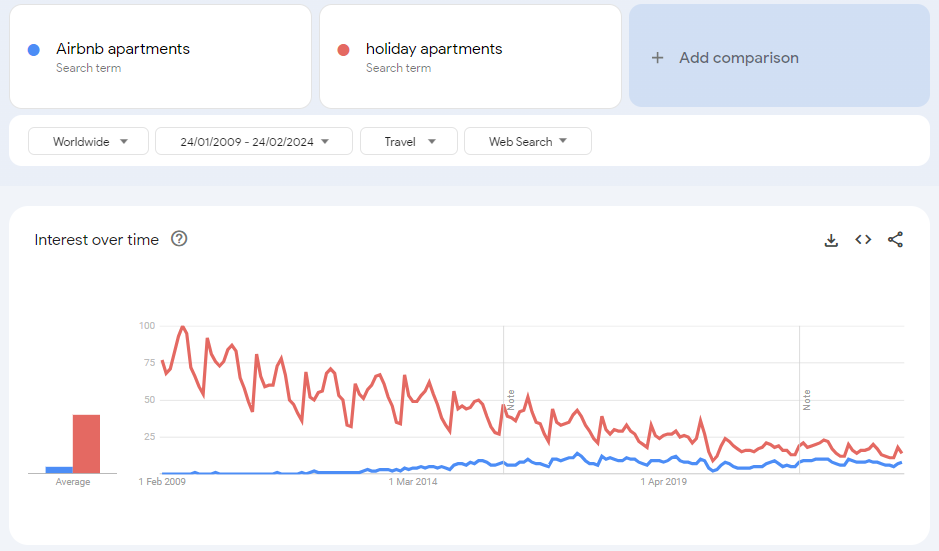

Google Trends helps determine trends, opportunities and risks. The graphs below show the stable search trends of the search word “Luxury Villa” and its comparative importance compared to others since 2004

This link will illustrate the trends over the last 20 years with various luxury search terms compared to “Luxury Villa” in global travel.

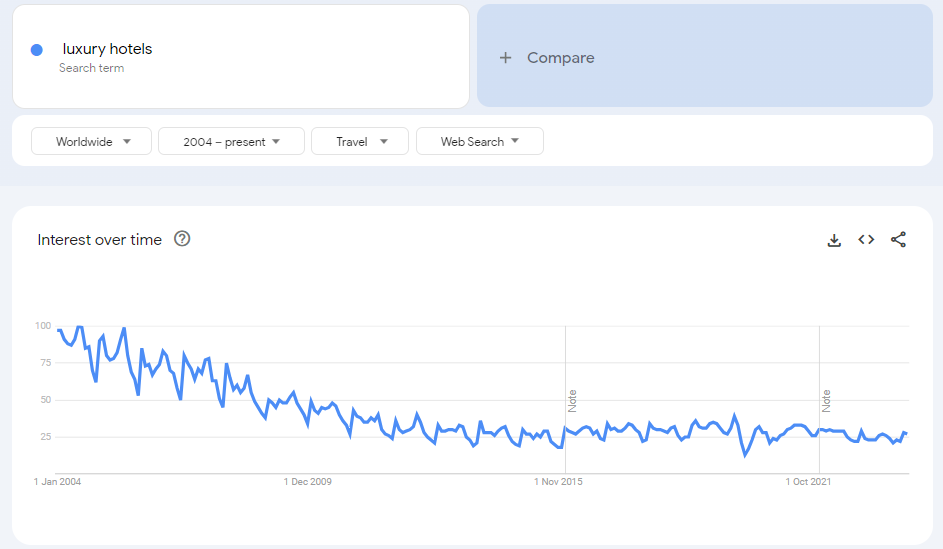

On the other hand, searches for Luxury Hotels have declined despite the overall trend and interest in the hospitality sector, which appears bizarre.

This is likely due to the significant investment in brand hotels like the Marriott.

This drop in search is undoubtedly due to the rapid growth of loyalty programs, apps, and third-party marketing platforms and reduced spend on Google and other search engines. This signifies prominent corporate branding, memberships, apps, loyalty-based programs, and less search focus.

However, searches on Google Trends for Ultra-Luxury result in the following message!

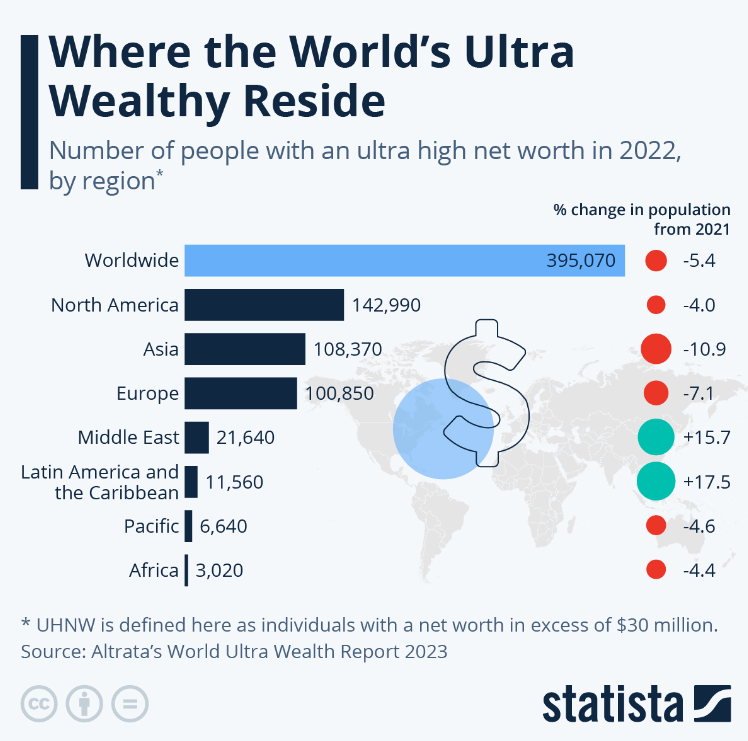

The number of Ultra Wealthy people has dropped.

According to Altrata's World Ultra Wealth 2023 report, there were a total of 395,070 ultra-wealthy individuals worldwide last year. This marked a 5.4 per cent decrease compared to the previous year, representing the first downturn since 2018. Concurrently, combined net worth also experienced a decline of 5.5 per cent, amounting to $45.4 trillion following several years of record highs.

North America retained its position as the region with the highest number of ultra-wealthy individuals, boasting 142,990. Asia followed closely in second place with 108,370 individuals, while Europe secured third place with 100,850 individuals.

Notably, Asia witnessed a substantial decline in its ultra-rich population, plummeting by 10.9 per cent in 2022. This marked the most significant proportional year-on-year drop among all global regions. Analysts attribute this decline to various factors, including the impact of China's stringent Covid policies and repercussions from the conflict in Ukraine. These factors led to disruptions in exports, consumption, and regional supply chains and a stock downturn, particularly in technology-driven markets like South Korea and Taiwan. Similarly, Europe experienced a notable decrease in its ultra-wealthy population during this period, recording a 7.1 per cent decline to 100,850 individuals.

The OTA brands are seldom ever booking “Ultra-Luxury” or even high value “Luxury” villas and chalets.

A global growth phenomenon, Airbnb, for example, acquired an extensive portfolio of luxury properties in 2017 under the Luxury Retreats banner and domain. Airbnb has never been recognised as a consistent marketer of quality accommodation, coming from the shared space business model and now having 7.7m listings.

VRBO is more recognised for larger family properties and is more likely to represent a higher percentage of higher-value bookings.

With its instant book and hotel approach to listings, Booking.com is the least likely to see luxury property bookings as a percentage of the total.

Full e-commerce is also less effective at high-value bookings, especially where conversations are often required, and ancillary and bespoke services are required. This can be seen below on the trend for generic holiday apartments as Airbnb converges with old search phrases and becomes the brand term.

6. Accommodation grading is not fit for purpose

In the rental industry, the properties and amenities are so diverse and distributed that it is almost impossible to grade them with a complete and well-defined ranking mechanism.

This is akin to hotels, which have historically had various schemes. Still, as online reviews took off, the diversity of “official” standards and limitations were not considered suitable.

Star Ratings

Hotel star ratings now appear to be a thing of the past in the public's eyes, despite several organisations still existing.

- AAA (American Automobile Association) – North America

- Australia: The Australian Star Ratings Scheme

- France: The Atout France agency

- Forbes Travel Guide.

- AA (Automobile Association) – United Kingdom

- DEHOGA (German Hotel and Restaurant Association) – Germany

- Tourism Grading Council of South Africa (TGCSA) – South Africa

- Hotelstars Union – Europe (an EU wide association)

- MICHELIN Guide – Global

- JTB (Japan Travel Bureau) – Japan

There are however various mechanisms for standardisation, matching spend to expectations. Some of these are covered below.

Mainstream from 1 to 5, Star Hotels

Plenty of hotels are still “Star Rated, but even the 20 countries that have implemented a unified rating system known as Hotelstars have different country rules.

For instance, two-star hotels are mandated to supply sewing and shoe polishing kits. Three-star establishments are expected to provide laundry and ironing services, while four-star accommodations must furnish guests with a 'bathrobe and slippers upon request'. To attain a five-star rating, hotels must offer personalised greetings for each guest, amenities such as fresh flowers or a gift in the room, and a turndown service, among other criteria.

However, there are notable exceptions to this scheme. France employs rating criteria based on factors like room and reception area size: for instance, double bedrooms must meet specific square footage requirements, ranging from nine square meters for a one-star hotel to 24 square meters for a five-star room.

In Italy, the standards are more generous, with a minimum room size of 14 square meters, although private bathrooms are not obligatory, potentially leading to shared facilities. Meanwhile, benchmarks differ across regions in Spain, another country not participating in the Hotelstars program.

Luxury Independent Hotels

Outside of hotel franchising brands and portfolio company ownership, top organisations overlay their membership with external or/and internal quality standards to match their client base requirements.

The three below are examples of external hotel brand standard organisations that are demanding when complying with their accreditation requirements for membership.

- Relais & Châteaux: 580 luxury hotels and fine-dining restaurants

- Small Luxury Hotels of the World is undoubtedly global, as its name would imply, but it’s not so small with 520 hotels.

- Leading hotels of the World comprised more than 400 hotels in over 80 countries, a collection of independent and uncommon luxury hotels.

Villas and Chalets (Hotel brand ownership)

Plenty of managers and marketing agents represent villa and chalet owners. There are thousands of properties with a thin veneer of luxury, booking at lower prices, with fewer concierge services and amenities, and often not in the best locations.

Hotel chains are adopting the best of these to amortise loyalty points and avoid loss of income in a growing vertical market. The three below are examples of brands owned by hotel chains that will have their standards for adoption.

These standards are less elevated and demanding due to the wide diversity of stock required for the vast customer bases but have hotel chain governance behind them.

- Onefinestay (an Accor hotel brand)

- Homes&Villas (a Marriott brand)

- Elite Havens (A Dusit brand)

Villas and Chalets (independent brands)

Below are three examples of independent rental brands from the hundreds worldwide that market more luxurious properties than the average holiday rental. These mid-range luxury properties are often available globally through OTAs as well. They are not formally graded by the marketing companies under a single badge, just internal and AI grading more recently.

7. Ultra Lux Villas and Chalet Standards

This is a group of properties with no standard brand or globally recognised collection. They are unique and stand aloft of all rentals before them.

Unlike the best hotels, no global or national brand exists in this sector. Generally, the rarefied atmosphere of the property and its guests excludes most booking platforms and organisations.

Matching these ultra-lux properties in incredible locations to the travel elite who respect and enjoy their privacy and quality of life requires skills and reach—a tailored, experienced, mature approach with a deep understanding of the market and rare networks. In effect, the black-book approach.

The well-articulated and researched Siretti Report highlights the growth of agents and travel specialists, particularly in the USA.

From surveying over 1000 HNWI and UNWI individuals, this report also emphasises that the self-booked approach has not materialised. This makes sense as busy people need help, and specialist knowledge is required.

Hotels and (U)HNWI can reach into collections of independently qualified accommodations such as Relais Chateaux and be re-assured of the experience, comfort and service. This is impossible in the rental world and relies on the expertise of those who went before them, as the private agent or travel expert relays.

As we have seen above, there are many “luxury” brands, but these properties are spread across multiple platforms and have no real diligence attached to the analysis of the listings. The selections are generally based on reviews, amenities and photo analysis. In other words, it is a scale approach to business.

8. Whale Sharks and UHNW Villas and Chalet Collections

The need for an exclusive listing portfolio.

Have you ever wondered how some of the world's rarest animals meet? Take the whale shark, a huge plankton-eating fish weighing up to 35 tons. They roam the oceans and rarely meet others, yet they survive. They are the elite fish of the seas.

However, anything from ten to five hundred whale sharks may gather anytime off the coasts of Australia, Belize, the Maldives, Mexico and more. These sites may be linked to a specific biological phenomenon – such as the spawning of land crabs at Christmas Island in the Indian Ocean, which provides whale sharks with the seasonal equivalent of a Christmas feast. No one knows when and where!

This may seem an unusual analogy, but they travel thousands of miles to mate and are both beautiful and incredibly rare. Ultra Lux accommodation is equally rare.

The best place to see whale sharks is when they collect together, but only those in the know, the lucky and rich, will ever witness it. With limited villas and chalets of this calibre and the same for UNWIs, it makes sense for there to become a collection that can be enjoyed and perused by those who can afford it! A source of rare accommodation.

There is a compulsive reason for the UHNWI and their agents to access a qualified and select brand of accommodation globally in one digital location underpinned by on-the-ground expertise and an acceptance grading. To be a member means exceptional properties, service and attitude.

Only a few can afford to stay; therefore, even the rich sometimes need to add marketing muscle to their beautiful homes, too; such is the rarity of the eco-system.

Although many may see this as a dilution of exclusivity and allowing potential UNWIs to compare and contrast, this is not a run-of-the-mill OTA approach or suggestion. The wealthy are global travellers, and distant reach and opportunity are at their fingertips.

This highly qualified members club would require validation of both accommodation and agents. It allows the aspirational and the newly wealthy to become part of something that drives business for those who need it and feeds back information across all industry elements.